Introduction

This case study illustrates how a financial institution resolved a loan default through arbitration proceedings facilitated on the PrivateCourt platform. By opting for an alternative dispute resolution (ADR) process, the claimant avoided prolonged litigation while ensuring a legally binding outcome.

Dispute Snapshot

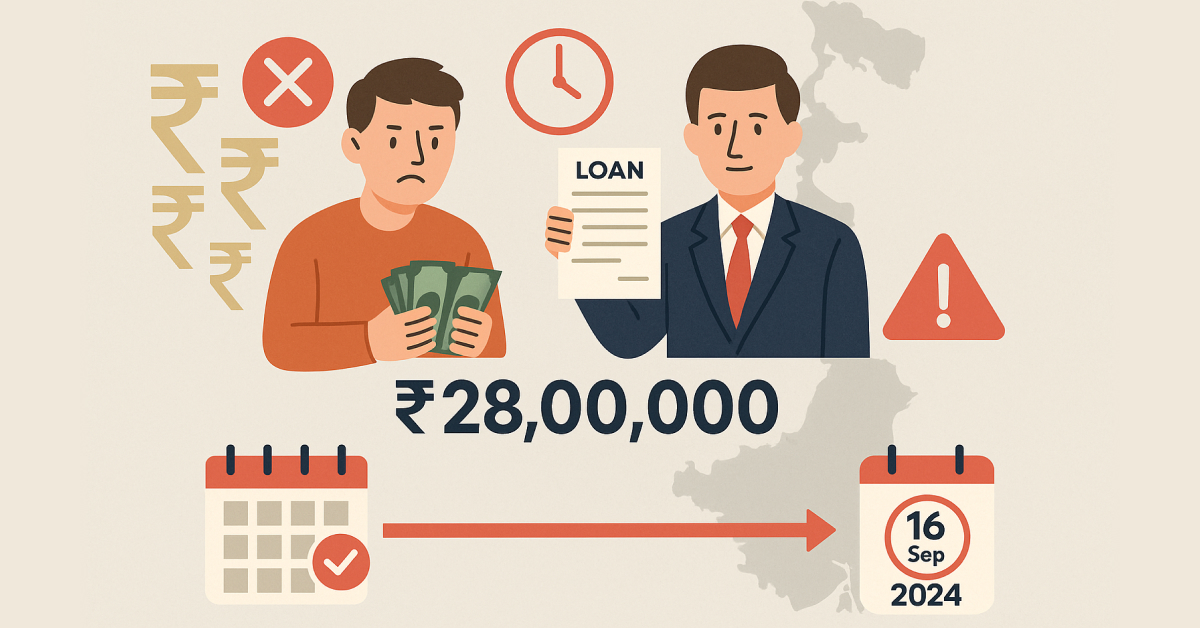

In 2023, a finance company sanctioned a loan of Rs. 28,00,000 to a borrower based in West Bengal. The terms of the agreement included a fixed repayment schedule through EMIs, commencing on 31 August 2023 and concluding on 28 February 2024.

While the borrower initially complied with the terms, defaults began to occur within a few months. Despite multiple reminders and follow-ups, the repayment ceased entirely. As of 16 September 2024, the unpaid amount had escalated to Rs. 1,67,600. With no resolution forthcoming, the lender invoked the arbitration clause included in the loan agreement to seek recovery through a legally enforceable process.

The Journey to Default

The borrower, operating a logistics-based SME, had secured the loan to support a new regional expansion plan. Initially, the funding was used to acquire vehicles and hire personnel for a large warehousing contract. However, a series of challenges soon disrupted operations. Payment delays from clients, an unexpected project cancellation, and rising operating costs weakened the business’s ability to maintain its EMI commitments.

Despite initial communication and verbal assurances, the borrower eventually stopped responding. Multiple notices, including a legal notice sent on 28 August 2024, failed to result in any meaningful engagement. Consequently, the claimant triggered the arbitration clause and initiated proceedings through the PrivateCourt platform.

Timeline of Key Events

| Date | Event |

|---|---|

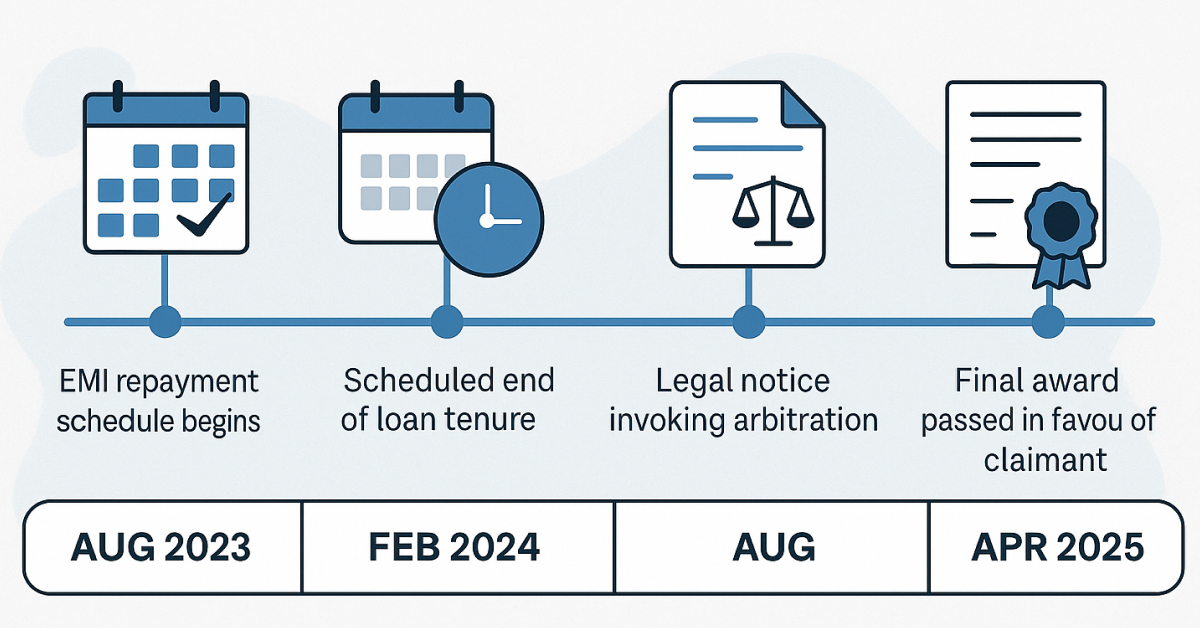

| 31 August 2023 | EMI repayment schedule begins |

| 28 February 2024 | Scheduled end of loan tenure |

| 28 August 2024 | Legal notice sent invoking arbitration |

| 5 September 2024 | The arbitrator appointed by the claimant under the agreement |

| 16 September 2024 | First virtual hearing held |

| 10 April 2025 | Final award passed in favour of the claimant |

The entire process was conducted digitally via the PrivateCourt platform, offering a streamlined and remote environment for dispute resolution.

Documentation and Submissions

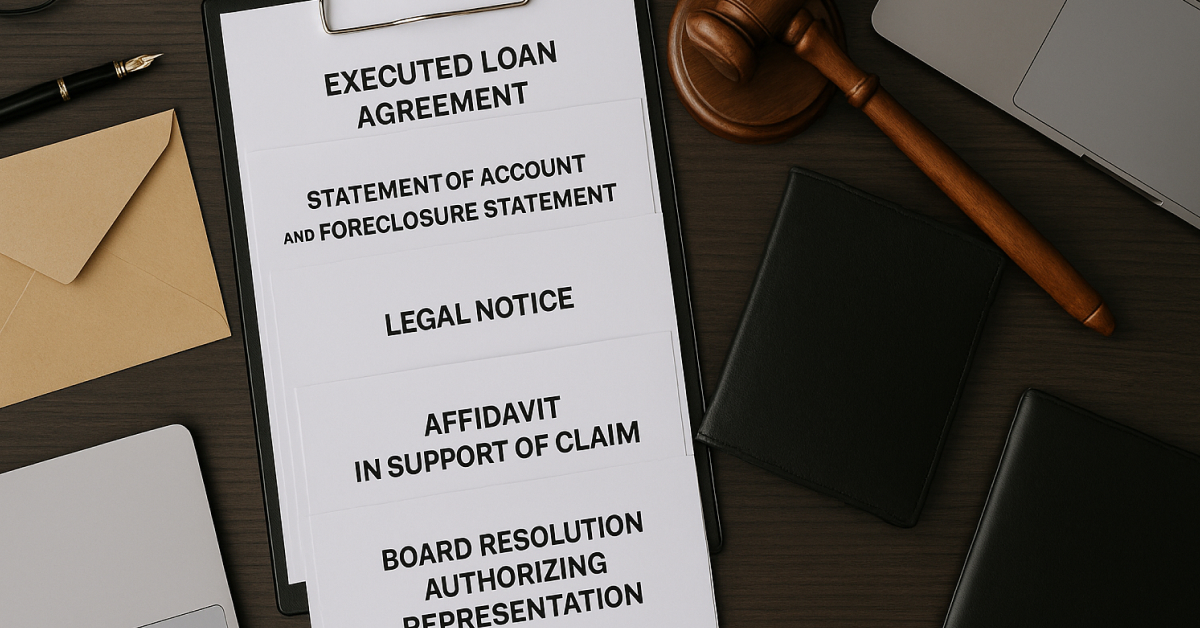

The claimant submitted the following documents during the arbitration proceedings:

- Executed loan agreement

- Statement of account and foreclosure statement

- Legal notice and delivery confirmation

- Affidavit in support of claim

- Board resolution authorizing representation

These documents established that the borrower had received the loan, agreed to the terms, and subsequently defaulted on the repayment schedule.

Arbitration Process Facilitated by PrivateCourt

Upon invocation of the arbitration clause, the claimant appointed a sole arbitrator in accordance with the terms of the agreement. PrivateCourt facilitated the arbitration proceedings by providing a digital platform for scheduling, communication, and document exchange.

Hearings were conducted virtually via video conferencing, with both parties given notice and opportunity to participate. While the respondent initially appeared, they chose not to file a statement of defence and did not actively engage in the subsequent proceedings.

The arbitrator followed due process under the Arbitration and Conciliation Act, 1996, evaluating the evidence and submissions presented by the claimant.

Final Award (Dated: 10 April 2025)

Based on the material available and the respondent’s failure to discharge the contractual obligations, the arbitrator issued the following award:

- The respondent is directed to pay Rs. 1,67,600 to the claimant

- Interest at 18% per annum is awarded from 16 September 2024 until realization

- Rs. 5,000 is to be paid as the cost of arbitral proceedings

The certified award was shared with both parties and is enforceable under the applicable provisions of Indian arbitration law.

Final Insights

This case demonstrates how the structured use of arbitration—facilitated by a neutral digital platform like PrivateCourt—can provide effective remedies for financial disputes. In just under seven months, a pending loan recovery matter transitioned from default to award, without entering the traditional court system.

PrivateCourt continues to offer technology-driven support to parties seeking a timely, enforceable, and compliant resolution to commercial disputes through ADR mechanisms such as arbitration and conciliation.

keywords: Loan Default, PrivateCourt, Arbitration, Online Arbitration, Dispute Resolution, Arbitration and Conciliation Act