Introduction

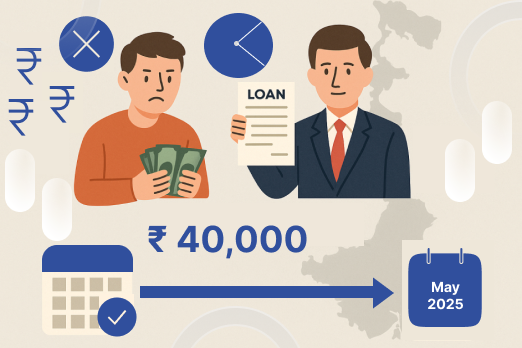

Retail entrepreneurs often rely on micro-loans to fund seasonal inventory and marketing surges. But when sales forecasts fail to match reality, repayment delays can turn into prolonged defaults. This case captures how a boutique retailer, burdened by a Rs. 40,000 default, was able to close the matter amicably using PrivateCourt’s seamless ADR platform. With legal enforceability, structured timelines, and platform neutrality, PrivateCourt enabled both parties to recover stability and financial clarity.

Dispute Snapshot

The respondent, a sole proprietor in the apparel retail business, had secured a short-term business loan to support festival season inventory buildup. However, post-season sales fell short due to local economic shifts and reduced foot traffic. Left with unsold goods and declining margins, the borrower began to miss EMI commitments. The lender initiated multiple follow-ups, which led to verbal assurances but no firm action. As default risks escalated, PrivateCourt’s ADR system was activated under the loan agreement’s resolution clause.

The Journey to Default

While the respondent initially maintained timely payments, the volatility in retail markets—compounded by supply chain delays and market fatigue—impacted business operations. Recurrent missed instalments signaled an inability to sustain repayment under original terms. The lender turned to PrivateCourt not only for recovery but also to maintain goodwill, knowing that mediation could offer a less disruptive solution. The borrower, feeling heard in a non-adversarial environment, agreed to a fair split-instalment resolution.

Timeline of Key Events

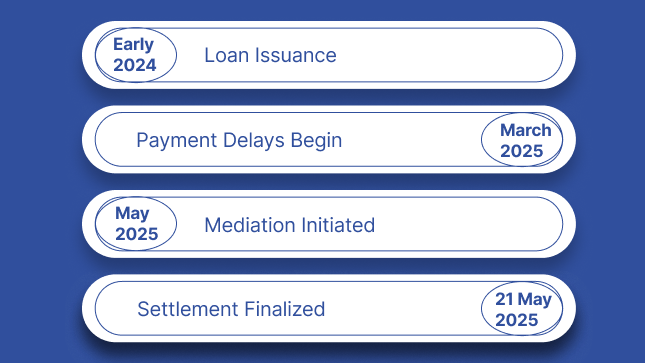

| Date | Event |

|---|---|

| Early 2024 | Loan Issuance |

| March 2025 | Payment Delays Begin |

| May 2025 | Mediation Initiated |

| 21 May 2025 | Settlement Finalized |

Documentation and Submissions

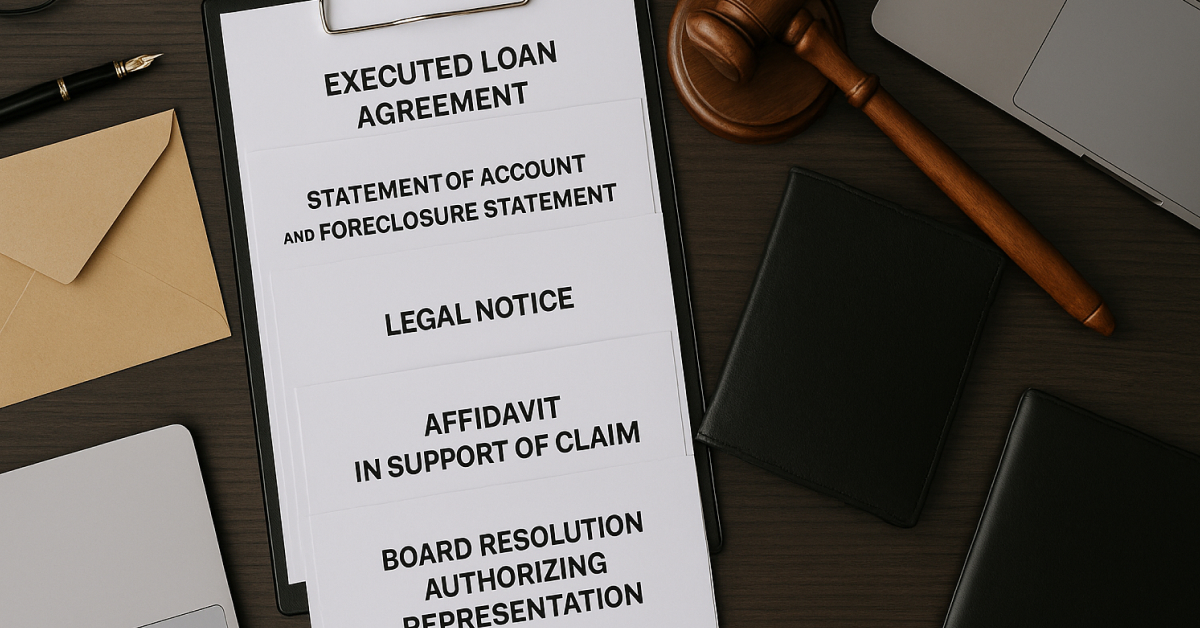

- Signed loan agreement and repayment schedule

- Notices issued for missed payments

- Borrower account statement

- Mutual acceptance of ADR process via PrivateCourt

- Recorded settlement terms

The ADR Process Facilitated by PrivateCourt

PrivateCourt facilitated virtual mediation via Zoom, allowing both parties to engage constructively. The mediator, trained in retail-sector dynamics, encouraged a resolution focused on achievability and transparency. The borrower proposed a split repayment of Rs. 20,000 each, to be cleared in two parts by 30 June 2025. This proposal was documented and confirmed by both sides, and fallback clauses were recorded to trigger arbitration if there was non-compliance.

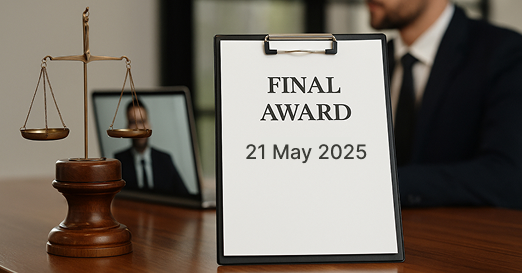

Final Award (Dated: 21 May 2025)

- Settlement Amount: Rs. 40,000/-

- Payment Terms: Two instalments of Rs. 20,000/- each by 30 June 2025

- Default Clause: Full loan revival with 18% interest if breached

Final Insights

PrivateCourt’s timely and industry-sensitive facilitation helped prevent a small dispute from becoming a reputational and legal burden. In just weeks, a growing loan default was translated into a firm repayment commitment, fully backed by enforceable digital records. For micro-retailers and digital lenders alike, PrivateCourt proved that ADR isn’t just an alternative—it’s the new standard for fair, efficient, and effective recovery.

keywords:Loan Default, PrivateCourt, ADR, Retail Loan, Mediation, Digital Resolution, Instalment Recovery