Introduction

In the fast-paced world of textiles, where demand surges and inventory moves in seasonal waves, cash flow disruptions can turn even a promising loan into a pending liability. This case involved a textile entrepreneur unable to clear nearly Rs. 1 lakh in outstanding dues. Traditional recovery mechanisms had hit a wall—until the lender opted to leverage PrivateCourt’s neutral and technology-enabled ADR platform. With a reputation for structured facilitation and swift resolution, PrivateCourt turned a dead-end dispute into a clear, enforceable one-time settlement, preserving business integrity and ensuring legal closure.

Dispute Snapshot

The respondent, a sole proprietor managing a small textile business, availed a working capital loan to restock fabric inventory ahead of an anticipated festive sales season. While the initial returns were encouraging, sales dipped post-season, leaving unsold stock and mounting operational expenses. Unable to rotate the capital and burdened by warehouse rent, the borrower started missing EMI commitments. With verbal assurances proving ineffective and legal action seeming premature, the lender triggered the ADR clause embedded in the agreement and approached PrivateCourt to mediate.

The Journey to Default

Despite good intent and early repayment discipline, the business faced unforeseen market conditions—leading to liquidity crunches. Loan servicing took a back seat as the respondent prioritized staff salaries and supplier obligations. The lender’s repeated follow-ups led to vague repayment promises that remained unfulfilled. Realizing the need for structured facilitation, the lender onboarded the case onto PrivateCourt’s ADR platform. Here, the borrower found a neutral and pressure-free environment to renegotiate the terms. PrivateCourt’s expert guidance reframed the situation, ultimately leading to an offer of a one-time foreclosure amount—making the path forward clear and consensual.

Timeline of Key Events

| Date | Event |

|---|---|

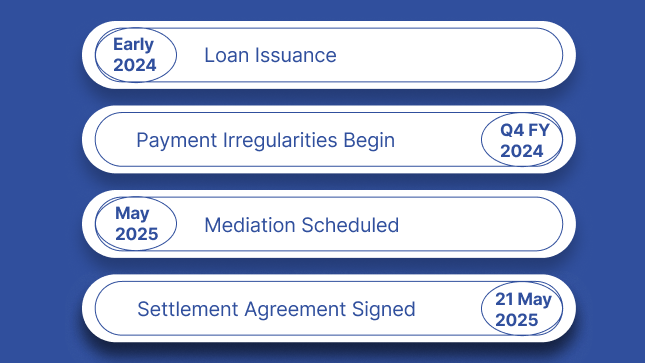

| Early 2024 | Loan Issuance |

| Q4 FY 2024 | Payment Irregularities Begin |

| May 2025 | Mediation Scheduled |

| 21 May 2025 | Settlement Agreement Signed |

Documentation and Submissions

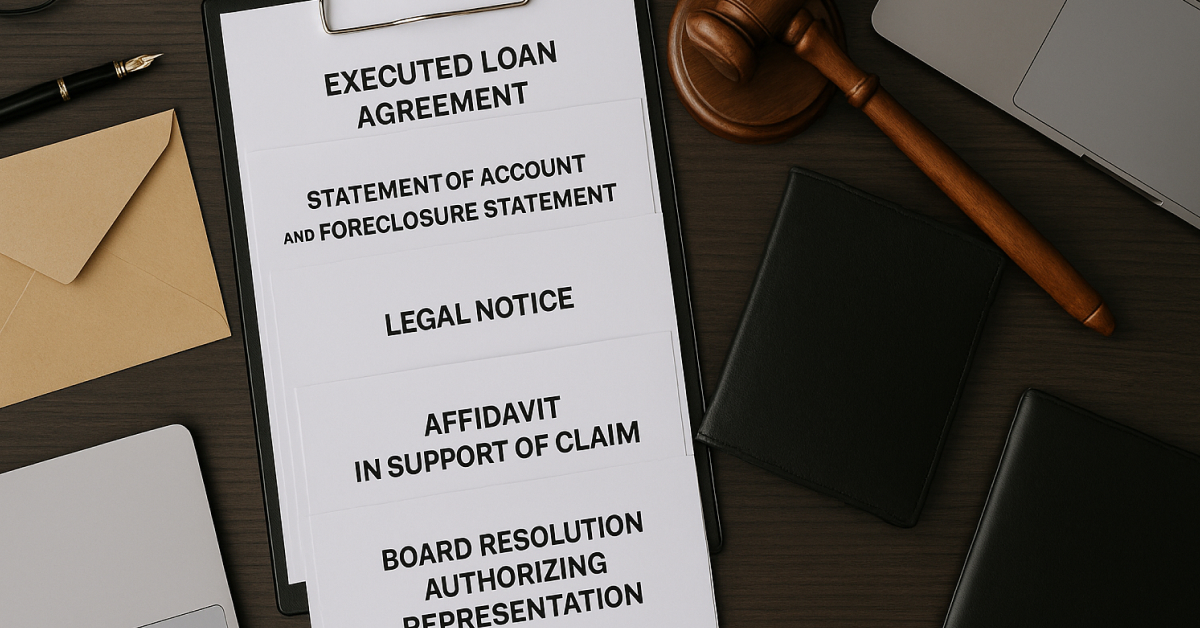

- Executed digital loan agreement

- Updated borrower account statements

- System-generated notices and digital correspondence logs

- Mutual consent forms for ADR participation

- Foreclosure proposal recorded and acknowledged via platform

The ADR Process Facilitated by PrivateCourt

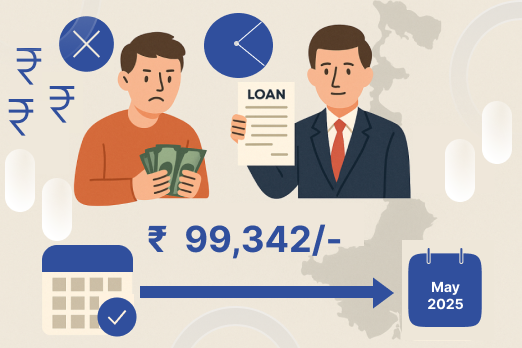

PrivateCourt coordinated the mediation digitally via its secure platform, allowing document exchange, negotiation, and recording of terms in a fully virtual environment. What made the difference was the platform’s structured, neutral tone—where the borrower was not just summoned, but invited to collaborate. The mediator guided both parties through a solution-focused dialogue. Ultimately, a one-time foreclosure amount of Rs. 99,342/- was agreed upon, with a payment deadline of 20 June 2025. An 18% default clause was built in for legal protection in case of non-compliance.

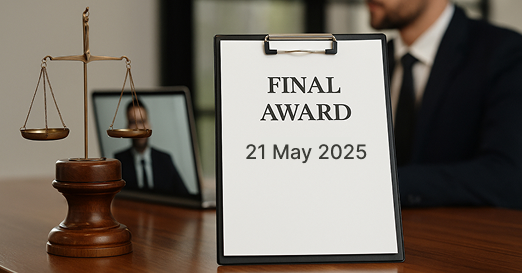

Final Award (Dated: 21 May 2025)

- Settlement Amount: Rs. 99,342/-

- Repayment Mode: One-time payment by 20 June 2025

- Default Clause: Revival of full claim with 18% interest upon breach

Final Insights

This case exemplifies the core strength of PrivateCourt’s ADR model—legal compliance, commercial sensitivity, and a human-first approach to conflict. The platform not only resolved a financial deadlock but also ensured that both sides walked away with clarity, confidence, and continued credibility. In high-turnover sectors like textiles, where agility is key, PrivateCourt’s digital-first resolution ensured time was saved, business reputation was protected, and justice was delivered without delay.

keywords:Loan Default, PrivateCourt, Textile Sector, ADR, Foreclosure Settlement, Online Mediation, Business Recovery