Introduction

In the ever-evolving realm of digital finance, lenders often find themselves at the crossroads of innovation and risk. While technology has accelerated access to financial services, it has also brought forth complexities in borrower relationships. This case presents one such scenario — a dispute between a registered finance company and two individuals who availed a business loan but allegedly defaulted within just a few months of disbursal.

Faced with non-repayment and uncooperative borrowers, the finance company turned to PrivateCourt, an online alternative dispute resolution (ADR) platform, seeking timely and neutral adjudication. What followed was a systematic, transparent, and legally grounded arbitration process that concluded within months, resulting in a definitive award. This case demonstrates the role of digital ADR in ensuring speedy redressal without compromising legal rigour or neutrality.

Dispute Snapshot

On December 20, 2023, a business loan agreement was executed between a digital finance firm and two individuals — one acting as a borrower (proprietor of a trading firm), and the other as a co-borrower. The sanctioned loan amount totalled Rs. 39.6 lakhs, with Rs. 33.91 lakhs being disbursed after standard deductions. The parties mutually agreed to repay the amount in two equal monthly instalments of Rs. 3.30 lakhs each, with an interest rate of 2% per month.

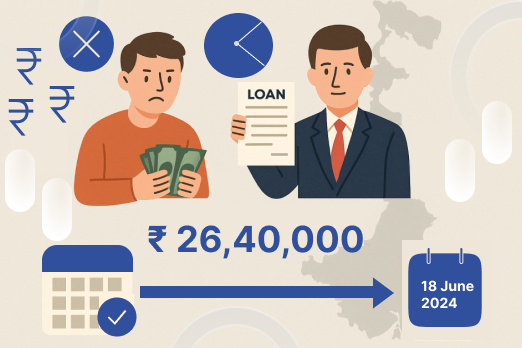

Despite the clear contractual terms and execution of all relevant documentation — including a loan application, sanction letter, bill of exchange, repayment schedule, and dispute resolution agreement — the repayment process derailed rapidly. By June 18, 2024, when the final instalment was due, the finance company had not received even a single complete EMI, prompting a claim of Rs. 26.40 lakhs along with interest and legal costs.

Notably, while the borrower initially appeared in the arbitration process and later defaulted in attendance, the co-borrower contested the claim altogether, alleging lack of consent, knowledge, or participation in the transaction — a claim later contradicted by documentation on record.

The Journey to Default

What began as a seemingly routine business loan turned into a contentious recovery challenge within a matter of weeks. The Claimant, a registered finance entity, had thoroughly vetted the loan request and processed disbursal only after receiving duly signed agreements from both parties. The loan was sanctioned with clearly defined EMI dates starting January 15, 2024, and ending June 18, 2024, supported by legally enforceable instruments such as a bill of exchange and a repayment schedule.

Despite these safeguards, the first signs of trouble appeared early. Neither of the two agreed instalments were paid in full, and repeated reminders from the Claimant went unanswered. Notices sent via registered post yielded no constructive response. Consequently, a legal notice and an invocation letter were issued on June 17, 2024, formally initiating the arbitration process under the Dispute Resolution Agreement.

During the proceedings, Opponent No. 1 (the borrower) raised concerns in the first hearing but then became completely non-responsive, ultimately leading the tribunal to proceed ex-parte against him. Opponent No. 2 (the co-borrower), however, contested the claim by denying any involvement, stating that she neither applied for nor received the loan, and was unaware of the transaction altogether. She further requested that her name be cleared from the credit bureau (CIBIL) records.

However, the Claimant countered these assertions with documentary proof, including a signed loan agreement, application forms, and communication records, establishing that both Opponents had full knowledge and had indeed executed the required documents. The tribunal reviewed all material evidence, including affidavits and electronic records, and concluded that both Opponents had breached their contractual obligations.

Timeline of Key Events

| Date | Event |

|---|---|

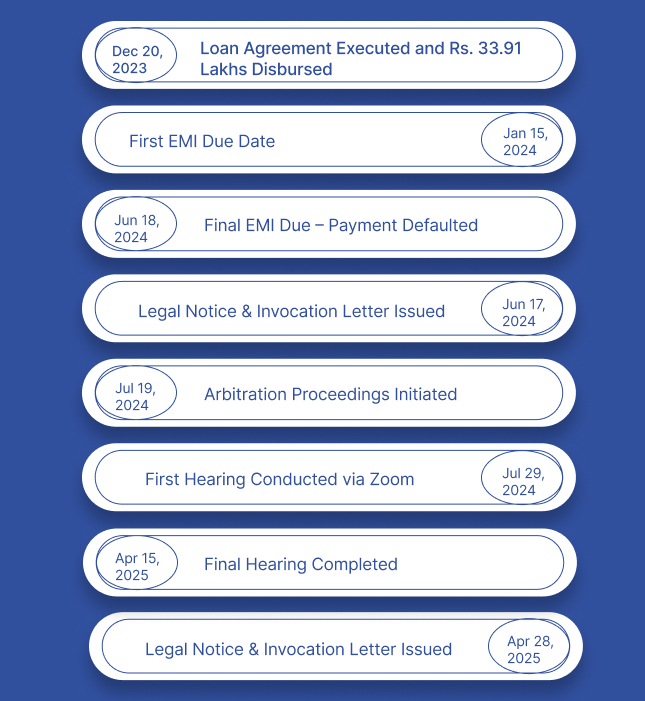

| Dec 20, 2023 | Loan Agreement Executed and Rs. 33.91 Lakhs Disbursed |

| Jan 15, 2024 | First EMI Due Date |

| Jun 18, 2024 | Final EMI Due – Payment Defaulted |

| Jun 17, 2024 | Legal Notice & Invocation Letter Issued |

| Jul 19, 2024 | Arbitration Proceedings Initiated |

| Jul 29, 2024 | First Hearing Conducted via Zoom |

| Apr 15, 2025 | Final Hearing Completed |

| Apr 28, 2025 | Final Award Passed by Sole Arbitrator |

Documentation and Submissions

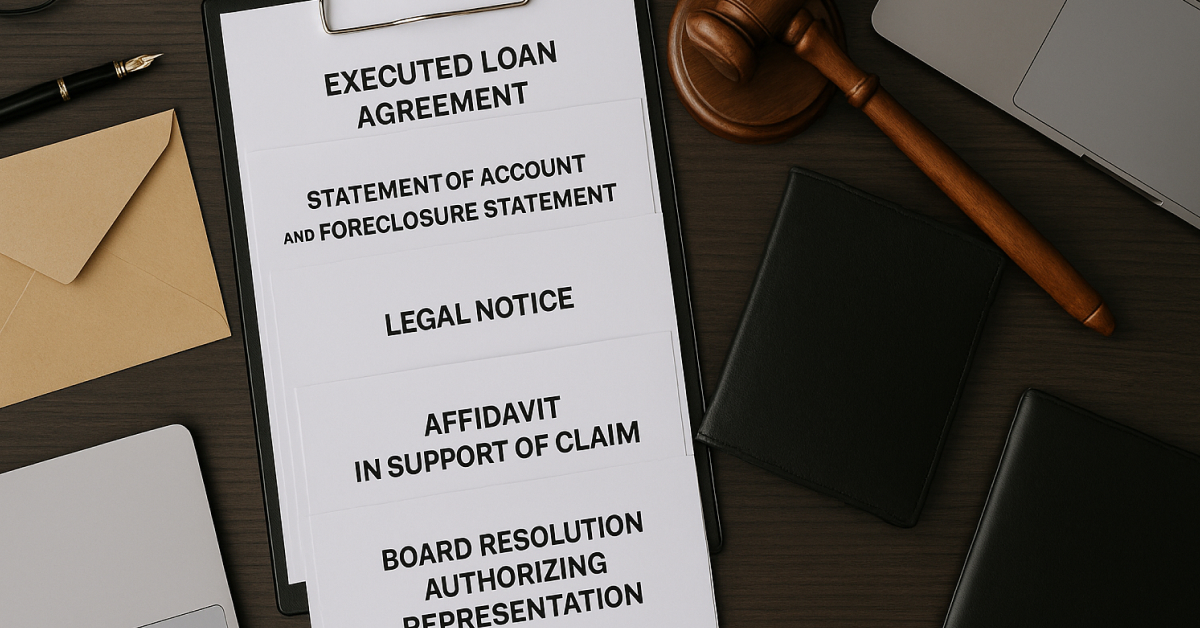

The Claimant submitted comprehensive documentation, including:

- Loan Application Form

- Sanction Letter

- Dispute Resolution Agreement

- Repayment Schedule & Bill of Exchange

- Legal Notice & Invocation Letter

- Affidavit in Support of Claim

- Statement of Accounts and Foreclosure Statement

- Board Resolution

Opponent No. 2 submitted a Statement of Defence, but provided no admissible evidence to support her claim of non-involvement.

Arbitration Process Facilitated by PrivateCourt

PrivateCourt acted solely as a neutral ADR platform, ensuring procedural integrity and full compliance with the Arbitration and Conciliation Act, 1996. Proceedings were conducted digitally via Zoom and administered with fairness by a Sole Arbitrator empaneled through PrivateCourt.

Final Award (Dated: April 28, 2025)

On April 28, 2025, the Arbitrator passed a speaking order holding the Opponents jointly and severally liable to:

- Pay Rs. 26,40,000/- to the Claimant

- Pay interest @2% per month from June 18, 2024, until the date of actual payment or recovery

- Bear arbitration fees of Rs. 2,000/- and legal expenses of Rs. 50,000/-

The award also emphasized that the Claimant had proven its case through documentary evidence and that the Opponents had failed to rebut the claims despite repeated opportunities.

Final Insights

This case is a textbook example of how digital arbitration platforms like PrivateCourt can bring resolution to commercial disputes in a legally sound and time-efficient manner. The ability to conduct hearings online allowed for logistical convenience, especially when parties ceased cooperation or defaulted.

The respondent’s cooperation, coupled with the claimant’s openness to settlement, allowed for a swift resolution through a consent award. PrivateCourt continues to empower NBFCs, banks, and MSMEs by offering online dispute resolution services rooted in compliance, convenience, and fairness.

keywords: Loan recovery dispute, ADR India,PrivateCourt arbitration, online dispute resolution ,commercial loan default , debt resolution and digital arbitration platform